European leveraged finance in 2023 was saddled with the negative effects of elevated interest rates. But as the market adjusts to the "new normal", rate and price stability offer hope for a brighter 2024.

European leveraged finance overview

Rising interest rates have pushed up borrowing costs and constrained issuance activity

Subdued M&A pipeline and cautious underwriting by banks limit buyout financing opportunities

Where transactions have progressed, the bulk of activity has been propelled by refinancing deals

Private credit proves resilient in the face of wider dislocation, attracting banks into the segment

Jumbo Worldpay financing shows that investor appetite for high-quality credits remains strong, with a potential warming for backdrop in 2024

After a slow year, market behaviour will mimic certain human traits, which will act as drivers in leveraged finance markets in 2024, as lenders and borrowers look to increase activity levels

Restlessness, imitation, creativity, distraction and optimism will, in their own way, each propel market participant activity levels

More banks may move to build out their private debt capabilities, imitating the successful private debt model that demonstrated its resilience through the current cycle

In a flat market, creativity will see lenders repurpose existing funding sources and develop new products to unlock liquidity

Among alternative assets, private debt has matured rapidly and is enjoying a 'golden moment' as a markedly attractive floating-rate product

In 2024, a mounting interest burden will give rise to novel debt structures for LBOs

As a typical credit is held by a single lender or small club, the private debt model enables providers to move more quickly than their peers

Not wishing to miss this golden opportunity, investment banks are quickly establishing or building up their private debt desks, introducing another valuable option to the funding mix

After a challenging period for sponsor deal activity and limited access to finance, the outlook for the year ahead is improving

Expectations of interest rate stability are raising hopes that pricing and modelling capital structures will be easier and allow gaps in pricing expectations between buyers and sellers to narrow

High levels of dry powder and unexited assets will put structural pressure on managers to do deals, improving prospects for deal financing pipelines

Private debt has gained market share and will remain a key part of the acquisition finance mix, but loan and bond markets are rallying, providing sponsors with a wider set of financing options

Rising interest rates have pushed up borrowing costs and constrained issuance activity

Subdued M&A pipeline and cautious underwriting by banks limit buyout financing opportunities

Where transactions have progressed, the bulk of activity has been propelled by refinancing deals

Private credit proves resilient in the face of wider dislocation, attracting banks into the segment

Jumbo Worldpay financing shows that investor appetite for high-quality credits remains strong, with a potential warming for backdrop in 2024

European leveraged finance has had a bumpy ride over the past 12 months. But after a difficult run, markets are hoping for more stable conditions in 2024.

Rising interest rates have had the single biggest impact on leveraged finance issuance through the course of 2023, with the European Central Bank (ECB) hiking rates to the highest levels observed since the turn of the century and the Bank of England (BoE) raising its base rate to a 15-year high.

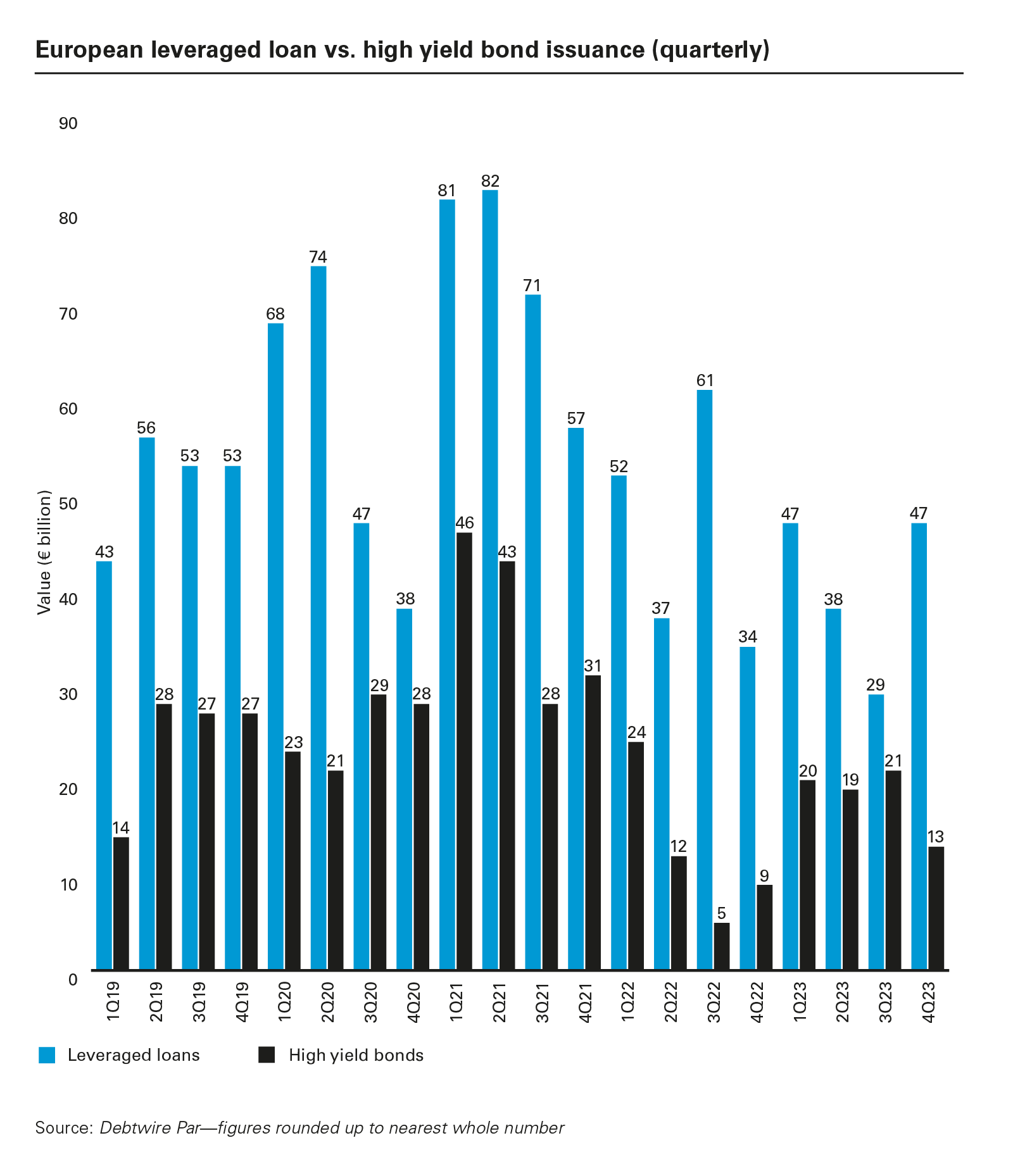

Borrowing costs have increased in line with rising rates, limiting issuers' ability to afford new debt facilities and making refinancing, unless pressing or opportunistic for the right issuers, unattractive. Issuance of floating-rate syndicated loan facilities has been hardest hit, with Debtwire figures showing a 10 per cent decline in European leveraged loan issuance in 2023 to US$193.9 billion compared to 2022.

The picture for European high yield bond issuance has been brighter. Issuance climbed 47 per cent in 2023 to reach US$79.4 billion, as issuers pivoted towards fixed-rate, high yield bonds over floating-rate syndicated loans in an unpredictable interest rate environment. But even though high yield bonds have offered more certainty on pricing, the double-digit rise in year-on-year issuance in 2023 has to be placed in the context of exceptionally low levels of high yield issuance in 2022.

When deals have progressed, the bulk of activity on leveraged capital markets has been driven by refinancing, with combined syndicated loan and high yield bond refinancing climbing 46 per cent in 2023 to account for 58 per cent of overall leveraged capital markets issuance.

In loan markets, large refinancings have included Nord Anglia (€1.51 billion), Leo Pharma (€1.35 billion) and BME Group (also €1.35 billion). Meanwhile big-ticket, high yield bond refinancings included gym chain Pure Gym, which raised €380 million in senior secured notes due in 2028 and priced at 8.25 per cent, and £475 million senior secured notes also due in 2028 and priced at 10 per cent. French-based television production Banijay secured a €450 million senior secured note and a US$500 million senior secured note to repay two existing outstanding high yield bonds in full.

Investors have been willing to refinance well-known credits, albeit at higher pricing, despite volatile markets.

Banks did clear the bulk of syndicated debt overhangs in 2023, which saw a cautious return to markets relative to 2022, but it has remained challenging for banks to underwrite new deals and take on syndication risk. This has contributed to a sharp decline in issuance for new-money buyout deals, with combined syndicated loan and high yield bond issuance for buyouts declining by 69 per cent year-on-year to just US$22 billion in 2023.

This has opened up opportunities for private debt franchises to continue building market share and finance larger transactions that may historically have been financed in syndicated loan or high yield bond markets.

According to Deloitte, jumbo financings supplied by direct lenders in 2023 have included packages for engineering materials company Envalior; pharmaceuticals company Dechra; and Swedish web hosting group One.com.

The ability of private debt funds to offer flexible financing packages, provide more leverage and to take and hold credits has helped to accelerate deal execution for borrowers in a choppy market and remove syndication risk.

Signs of stability as market looks to 2024

Looking ahead to 2024, there are some positive signs that loan and bond markets are beginning to stabilise after a challenging few months.

Inflation in the UK and Europe has started to slow, and after months of consecutive hikes there are signals that the ECB and BoE will keep rates stable, or even reduce rates, in 2024. The US Federal Reserve has also signalled that the cycle of rising interest rates is peaking.

How exactly monetary policy will evolve in the year ahead remains to be seen, but with rates at least levelling off towards the end of 2023, loan and bond pricing has settled.

69%

The decline in buyout deal value in Europe in 2023, year-on-year

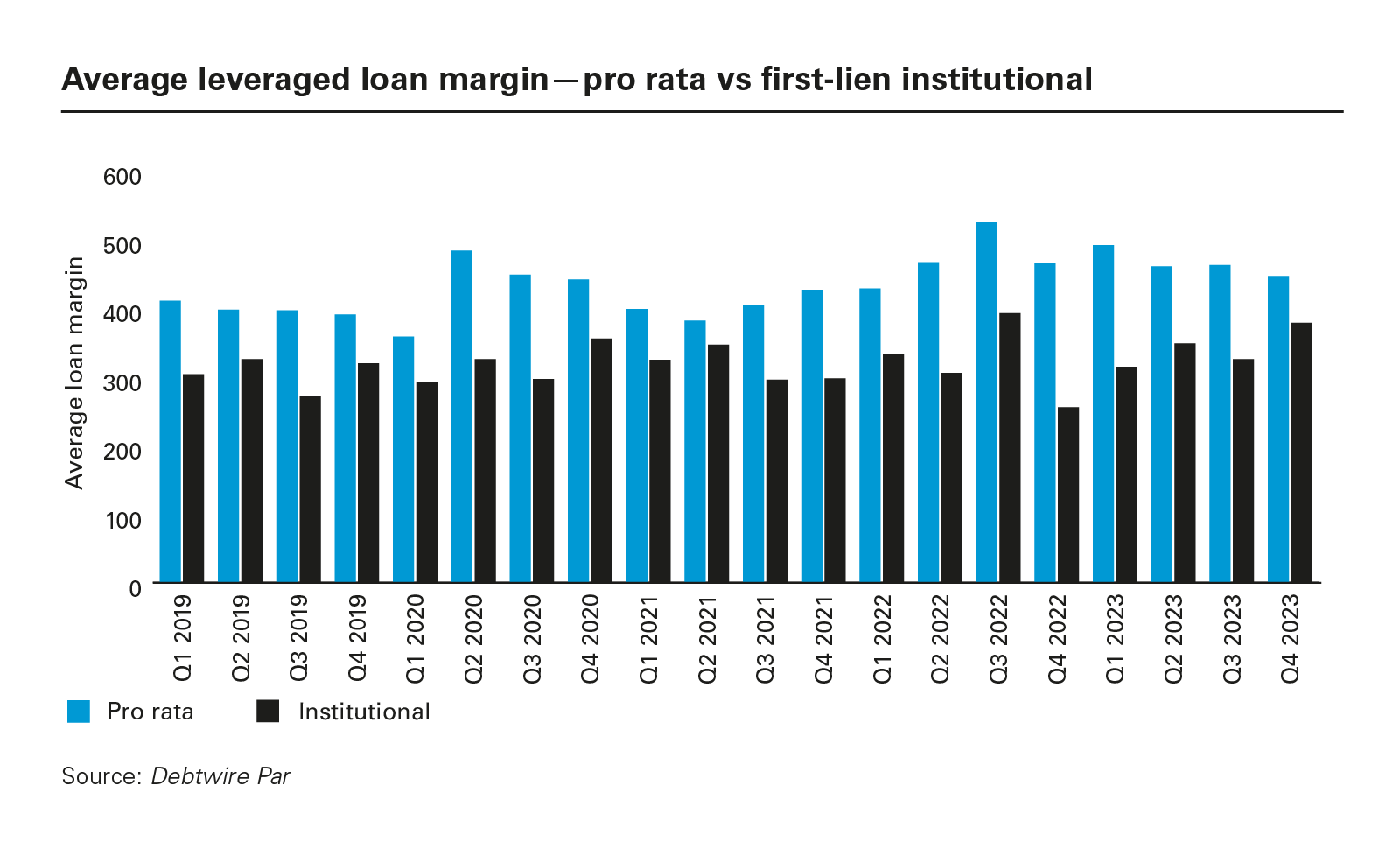

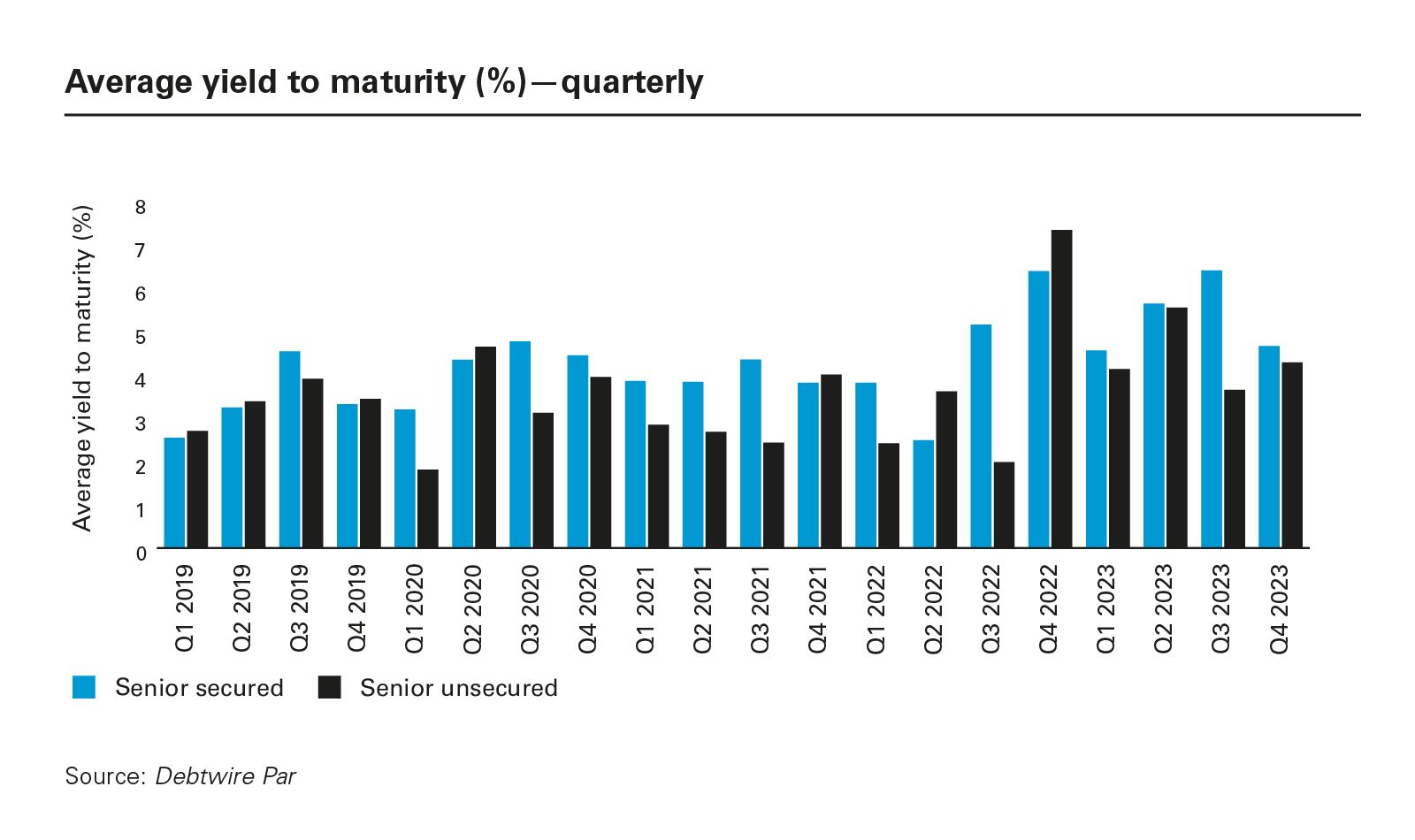

According to Debtwire, average margins on first-lien institutional loans reached 4.64 per cent in Q3 2023, down on the 5.23 per cent figure recorded in the same quarter last year. High yield bond yields have also eased over the course of 2023, down by approximately 3 per cent from the highs recorded at end-2022. Secondary market pricing has also settled, as have original issue discounts, giving issuers and lenders a firmer foundation when pricing risk.

The mega-deal financing of GTCR's buyout of US-based payments company Worldpay in the early autumn also sparked hopes that markets could reopen in force, with the company securing an US$8.65 billion loan and bond package that was oversubscribed as well as securing favourable borrower terms. Lenders and borrowers, however, did not get carried away after the Worldpay financing, and markets have remained cautious since that breakthrough deal.

Markets are by no means out of the woods. According to Fitch Ratings, European leveraged finance default rates are expected to edge higher in 2024 and 2025 to approximately 4 per cent as more credits approach maturities. Amend-and-extend, debt buybacks, and other liability management exercises are also expected to continue looming over the market.

In the face of these ongoing headwinds, leveraged capital markets may not have a banner year in 2024, but with interest rates and pricing stabilising, and markets adjusting to the "new normal" of higher rates and more selective lenders, the next 12 months should be better than the preceding 12.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

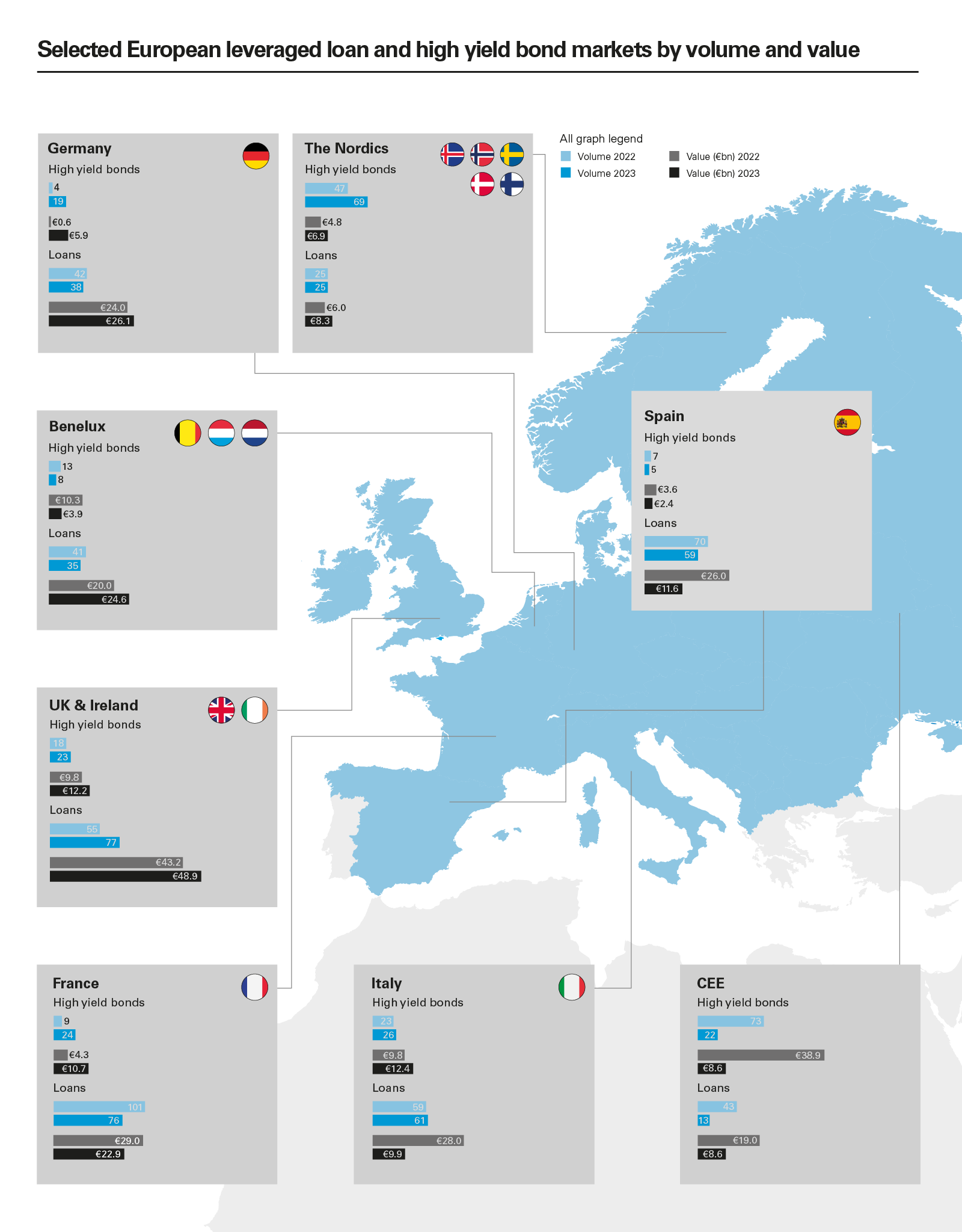

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: European leveraged loan vs. high yield bond issuance (quarterly) (PDF)

View full image: European leveraged loan vs. high yield bond issuance (quarterly) (PDF)

View full image: Average leveraged loan margin—pro rata vs first-lien institutional (PDF)

View full image: Average leveraged loan margin—pro rata vs first-lien institutional (PDF)

View full image: Average yield to maturity (%)—quarterly (PDF)

View full image: Average yield to maturity (%)—quarterly (PDF)