European leveraged finance in 2023 was saddled with the negative effects of elevated interest rates. But as the market adjusts to the "new normal", rate and price stability offer hope for a brighter 2024.

European leveraged finance overview

Rising interest rates have pushed up borrowing costs and constrained issuance activity

Subdued M&A pipeline and cautious underwriting by banks limit buyout financing opportunities

Where transactions have progressed, the bulk of activity has been propelled by refinancing deals

Private credit proves resilient in the face of wider dislocation, attracting banks into the segment

Jumbo Worldpay financing shows that investor appetite for high-quality credits remains strong, with a potential warming for backdrop in 2024

After a slow year, market behaviour will mimic certain human traits, which will act as drivers in leveraged finance markets in 2024, as lenders and borrowers look to increase activity levels

Restlessness, imitation, creativity, distraction and optimism will, in their own way, each propel market participant activity levels

More banks may move to build out their private debt capabilities, imitating the successful private debt model that demonstrated its resilience through the current cycle

In a flat market, creativity will see lenders repurpose existing funding sources and develop new products to unlock liquidity

Among alternative assets, private debt has matured rapidly and is enjoying a 'golden moment' as a markedly attractive floating-rate product

In 2024, a mounting interest burden will give rise to novel debt structures for LBOs

As a typical credit is held by a single lender or small club, the private debt model enables providers to move more quickly than their peers

Not wishing to miss this golden opportunity, investment banks are quickly establishing or building up their private debt desks, introducing another valuable option to the funding mix

After a challenging period for sponsor deal activity and limited access to finance, the outlook for the year ahead is improving

Expectations of interest rate stability are raising hopes that pricing and modelling capital structures will be easier and allow gaps in pricing expectations between buyers and sellers to narrow

High levels of dry powder and unexited assets will put structural pressure on managers to do deals, improving prospects for deal financing pipelines

Private debt has gained market share and will remain a key part of the acquisition finance mix, but loan and bond markets are rallying, providing sponsors with a wider set of financing options

After a challenging period for sponsor deal activity and limited access to finance, the outlook for the year ahead is improving

Expectations of interest rate stability are raising hopes that pricing and modelling capital structures will be easier and allow gaps in pricing expectations between buyers and sellers to narrow

High levels of dry powder and unexited assets will put structural pressure on managers to do deals, improving prospects for deal financing pipelines

Private debt has gained market share and will remain a key part of the acquisition finance mix, but loan and bond markets are rallying, providing sponsors with a wider set of financing options

Over the past 12 months, financial sponsors have been confronted with one of the toughest deal financing markets since the 2008 financial crisis. But, as interest rates stabilise, brighter days may be on the horizon.

Elevated interest rates—which have climbed to a 15-year high in the UK, and the highest levels in the European Union since the launch of the euro in 1999 —have had a significant impact on leveraged buyout deal structures.

Making the leveraged finance model work in an environment where capital costs have been rising, but where the vendors of high-quality companies have been reluctant to sell at discounted valuations, has been difficult for sponsors, who have had to be more careful about when to transact and which assets to target.

69%

The decline in buyout deal value in Western Europe in 2023, according to Mergermarket data

This gap between buyer and seller valuation expectations has had a chilling impact on transaction and deal financing activity. According to Mergermarket data, Western European buyout deal value declined by more than two-thirds (69 per cent) in 2023.

The double-digit slide in buyout value has meant limited buyout financing transaction flow, with Debtwire Par figures highlighting cratering syndicated loan financing for buyouts, which has fallen by more than 73 per cent in 2023. High yield issuance for buyouts has fallen by a third over the same period.

Improving outlook as rate rises peak

However, as grim as the headline numbers for buyout transactions and buyout financing have been in 2023, there is cautious optimism that conditions for dealmaking and deal financing will improve in the year ahead.

Hopes for a rally in activity in 2024 come as signs emerge that central banks are approaching the end of the recent cycle of rate hikes. After raising interest rates consistently during the preceding 18 months, the US Federal Reserve, ECB and BoE all stopped hiking at their most recent meetings, raising expectations that interest rates have reached their peak.

Even if rates remain at current elevated levels over the medium to long term, as several economists anticipate, a clearer picture on where interest rates will settle will give financial sponsors comfort when pricing deals, modelling appropriate leverage levels and, ultimately, in determining how close to sell-side price expectations they are willing to get.

The private equity industry is now more than 40 years old, and the model has worked in periods where interest rates have been higher than they are now. As interest rates have been so low for so long and debt has been freely available on attractive borrower-friendly terms as to leverage and otherwise, it has taken more time for buyer and seller pricing expectations to recalibrate and converge than in previous cycles. Interest rate stability will go a long way toward building a consensus around realistic capital structures for acquisitions, putting buyers and sellers back in sync.

The building pressure on private equity firms to transact will also be a strong factor driving activity in 2024. According to Bain & Co analysis, there is a record US$1.1 trillion of uninvested dry powder sitting in buyout funds, with buyout firms also holding an all-time high US$2.8 trillion worth of assets in portfolios—more than quadruple the levels seen during the 2008 financial crisis. After a slow year for dealmaking in 2023, the clock is ticking—deals will have to be brought to the table.

Another driver of activity in the sponsor market will be refinancing and managing assets that require new capital structures.

For companies that have traded well through the past 12 to 24 months and/or are in popular sectors, refinancing markets have been very much open, as seen in the case of deals like Pure Gym and Zentiva Group, which enjoyed strong support from investors.

Debt costs have increased, but within manageable thresholds, and investment banks have been ready to put together refinancings for familiar credits on a best-efforts basis. It has been easier for arranging banks to support refinancings on best efforts than to provide the underwritten commitments required for new deals. Interest rate headwinds may be easing, but there is still a degree of caution around syndication risk after many banks found themselves exposed to debts that ended up stuck in syndication a year ago.

There is another cluster of sponsor-backed companies, which took on high levels of leverage at near-zero interest rates, that will find it challenging to refinance existing capital structures in the current environment. In these scenarios, sponsors will have the option of either paying a fee to lenders to amend-and-extend the terms on current borrowings, or look to sell on the asset in an M&A deal to a new owner that can put a new capital structure in place.

As the market reopens for new deals, and momentum behind refinancings continues to build, sponsors will keep all their options open when deciding on what financing routes to go down.

If loan and bond markets continue to rebound, offering sponsors lower capital costs, more deals will start to revert to these funding pools. This could put pressure on private debt funds to reduce pricing in order to retain the market share won during the past two years, introducing a new competitive dynamic into the financing space.

The dislocation in syndicated loan and high yield bond markets during the past 18 months has provided a window of opportunity for private debt lenders. These creditors have expanded beyond the mid-market and are becoming credible options for large-cap credits, which previously would have turned immediately to the syndicated capital markets when seeking financing.

As the sponsor market emerges from a period of volatility, the private debt model is well placed to continue increasing its market share, providing sponsors with flexible financing packages and speedy deal execution with no syndication risk. One caveat to that is the emergence of private debt club deals where, although there may be no syndication risk, the challenge of assembling the club on aligned underwritten terms should not be underestimated and can affect speed of execution.

It will be interesting to observe how private debt lenders respond as investor and bank appetite for Term Loan B and high yield bonds rallies.

Early signs that syndicated loan and high yield bond markets are coming back to life for new buyout deals emerged in the late summer of 2023, as GTCR secured an US$8.65 billion bond and loan package to finance its carve-out of payments company Worldpay. According to the Financial Times, investors placed orders in excess of US$20 billion for the debt, enabling Worldpay to upsize the term loan part of the package from a starting point of US$3.4 billion to US$5 billion, and to reduce interest rate margins down from 3.75 per cent to 3 per cent.

If loan and bond markets continue to rebound, offering sponsors lower capital costs, more deals will start to revert to these funding pools. This could put pressure on private debt funds to reduce pricing in order to retain the market share won during the past two years, introducing a new competitive dynamic into the financing space.

After a challenging period, deal activity and financing optionality may finally be opening up for sponsors again.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

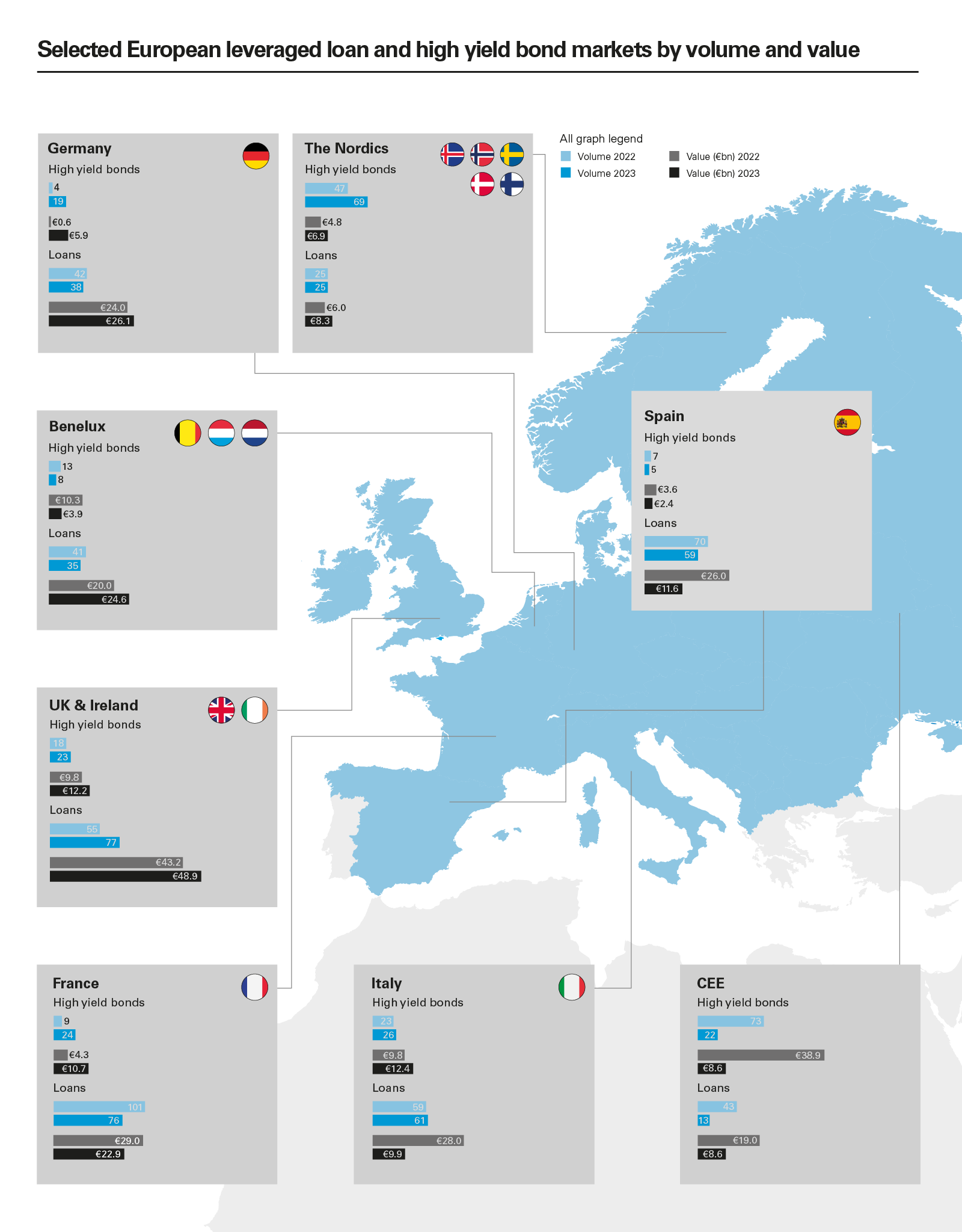

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

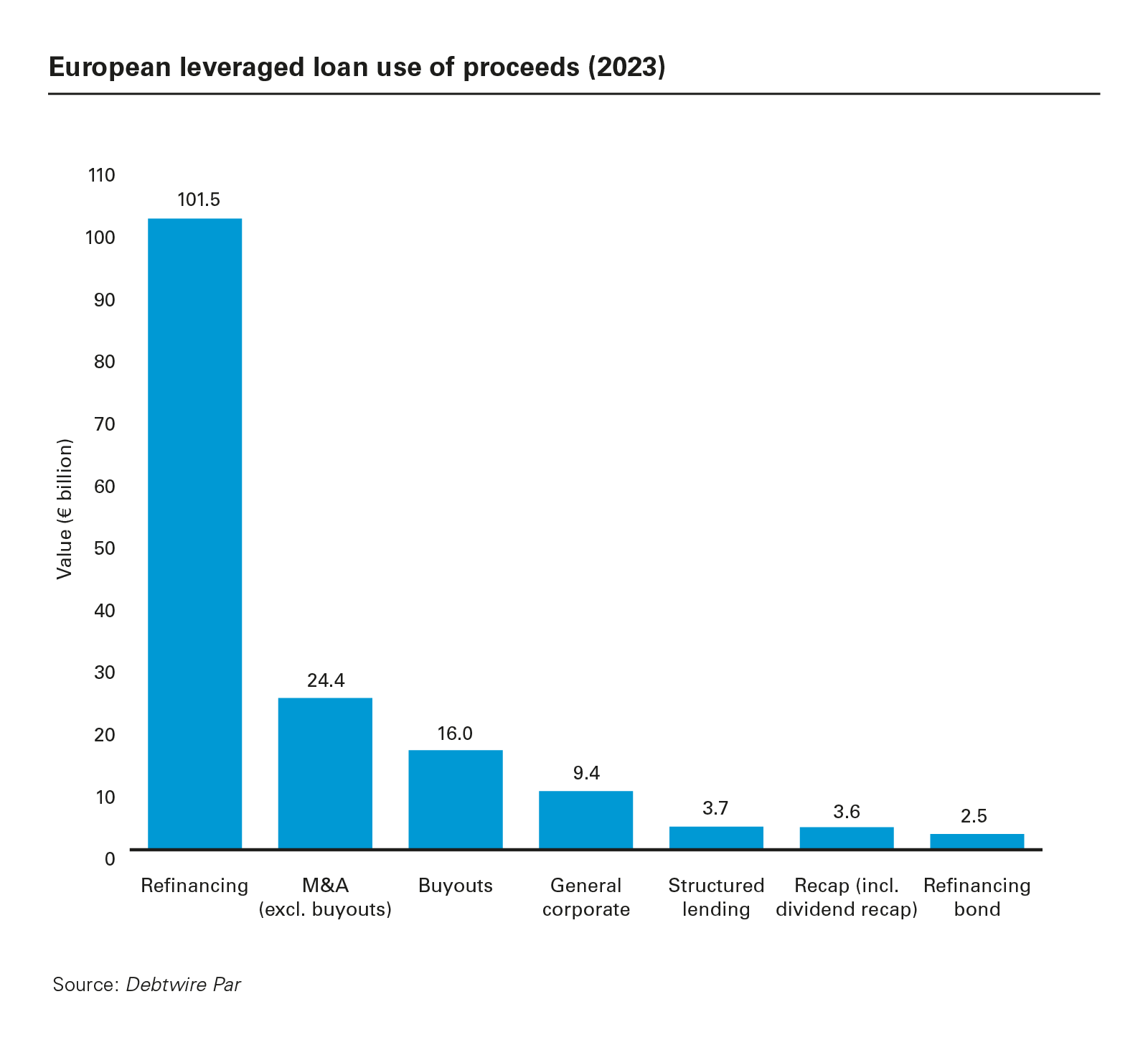

View full image: European leveraged loan use of proceeds (2023) (PDF)

View full image: European leveraged loan use of proceeds (2023) (PDF)

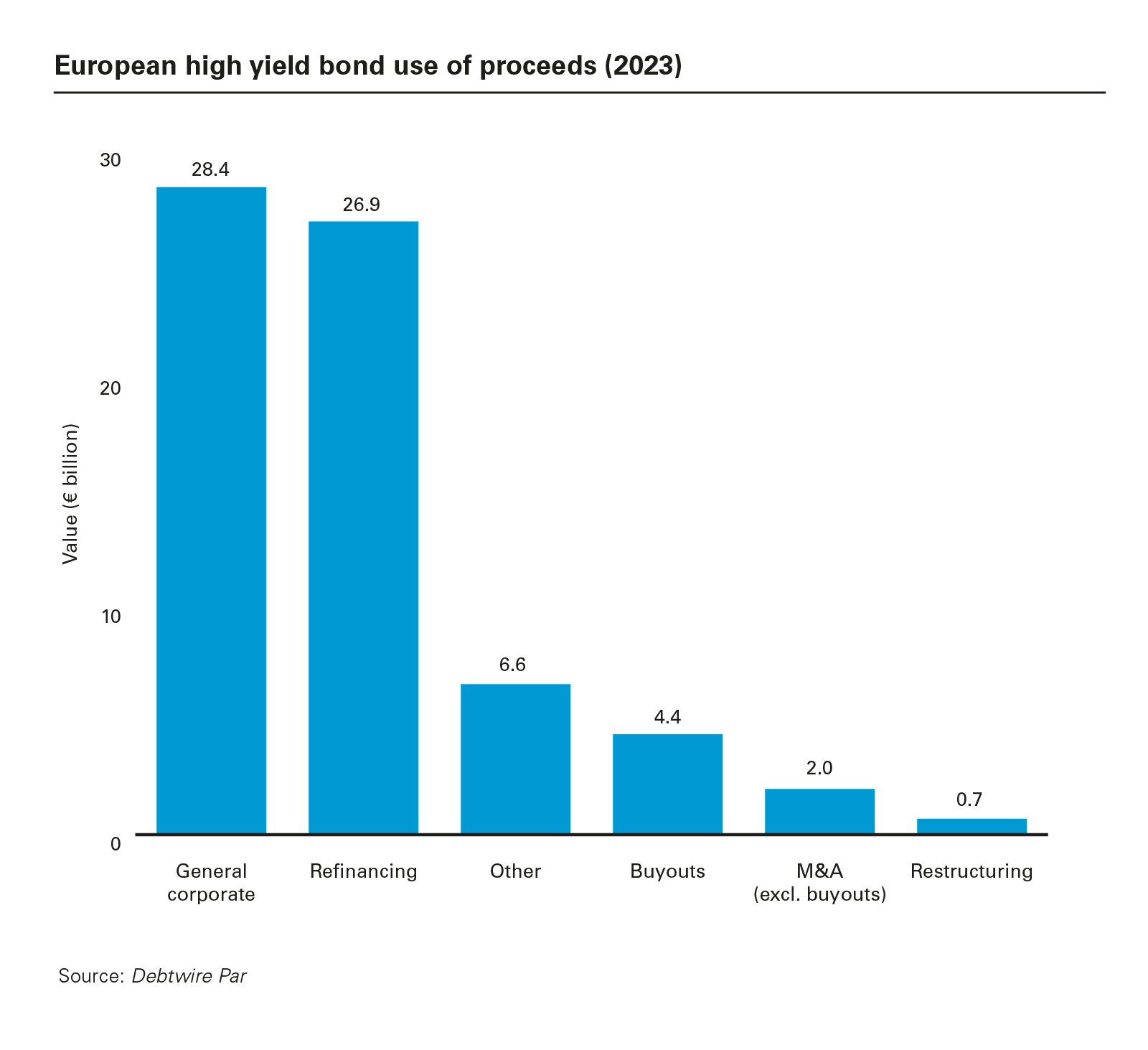

View full image: European high yield bond use of proceeds (2023) (PDF)

View full image: European high yield bond use of proceeds (2023) (PDF)

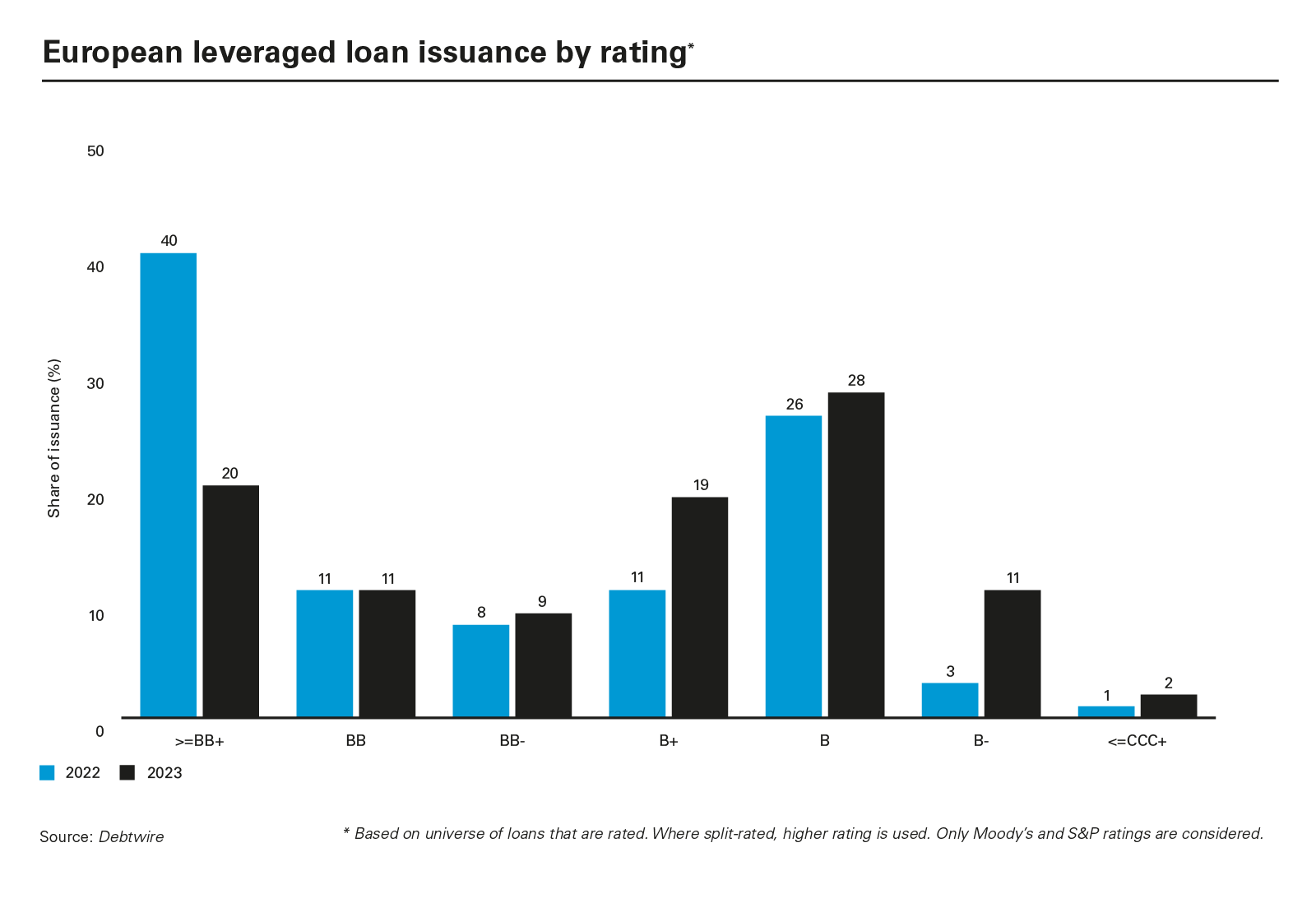

View full image: European leveraged loan issuance by rating* (PDF)

View full image: European leveraged loan issuance by rating* (PDF)